According to a survey by TransUnion, a Canada-based credit reporting agency, 60 percent of Canadians said they were targeted with online, email, phone call, or text messaging fraud in the last three months, of which 10 percent fell victim.

Finding the right rental home is supposed to be exciting but in today’s busy housing market, it can be overwhelming and full of risks. The rise of online platforms and digital transactions has made finding the perfect place more convenient than ever. However, along with this convenience comes the risk of rental scams, which can leave unsuspecting tenants financially devastated and emotionally distraught. Manjunath Chandramma, a newcomer from India, experienced such a scam upon moving to Canada.

Manjunath arrived in Toronto in November 2022, looking for a place to stay. He found a listing in Hamilton for a master bedroom in a house, offered at $1,000 per month. As a newcomer, he was eager to settle in and paid $1,500 upfront to the Brampton-based couple who owned the property. However, upon arrival, he discovered the house had no electricity. The landlord promised it would be fixed soon, but as evening came, Manjunath was left in the cold darkness.

The situation escalated when the landlord, instead of addressing the issue, berated Manjunath for his inquiries and ultimately demanded that he vacate the premises or endure the night without electricity. Unable to stay in the dark and cold, he agreed to vacate the house. The owner came and took the house keys back from him. When asked about his $1,500, the owner said he had exhausted his daily transaction limit and will transfer the amount the next day.

With no other option, Manjunath had to vacate the house, leaving behind his deposit. Despite numerous attempts to retrieve his full deposit, Manjunath lost $1,000 in that one day. The landlord's responses ranged from excuses to outright hostility, leaving Manjunath feeling cheated and vulnerable in a new country in a foreign land. The promised reimbursement of $1,500 dwindled to $500, with the landlord citing baseless reasons and resorting to emotional manipulation.

Manjunath's ordeal serves as a cautionary tale, highlighting the importance of vigilance and awareness when navigating the rental landscape in Canada. Unfortunately, rental scams are not uncommon, and unsuspecting tenants can easily fall victim to unscrupulous practices that exploit their trust and vulnerability.

So, how can individuals safeguard themselves against such fraudulent schemes? Here are the few things to remember while renting a house:

Research and verify the property and owners: To safeguard oneself from scam, it is crucial to verify the authenticity of listings and owners. Before committing to any rental agreement, search for the property and owner names online to see if any discrepancies in the information you were given or any issues pop up. Also, you can ask to see the property tax bill to confirm ownership and request the name and contact information of previous tenants to secure references. Any genuine landlord should feel comfortable sharing this information.

“One prevalent scam is the phantom rental scheme, where fraudsters advertise properties that either don't exist or are not available for rent. They often lure unsuspecting victims with enticingly low prices or attractive amenities. To avoid falling victim to such scams, it is crucial to conduct thorough research,” says Chris McGuire, founder of Real Estate Exam Ninja.

The scamsters also use “bait-and-switch” tactic where they advertise a desirable property at an attractive price, only to switch it with a less appealing one once you are interested, shares Samantha Od, Real Estate Sales Representative and Montreal Division Manager at Precondo. “Always be cautious if a landlord seems too eager to rush you into signing without proper documentation. Take your time to review the terms and conditions, ensuring they align with what was initially presented,” she says.

Conduct a physical inspection: Another important point to keep in mind before renting a property is inspecting it in person to assess its condition and ensure that it meets your expectations and requirements. “Always insist on physically visiting the property before making any payments or signing a lease agreement. Be wary of landlords who are reluctant to meet in person or demand cash-only transactions,” says Mcguire who is also a licensed broker.

Always meet the landlord or agent in person at the rental property, or at least view it through a video tour if you are renting from abroad, before making any payments or providing personal information. There is greater risk if you are renting from abroad. Under these circumstances, you want to ensure to research both the owner and the address and to get and check references for the landlord. When connecting with the references, conduct a simple internet search on them in advance and consider asking questions that will enable you to ensure they lived at the property.

Avoid Rental Deposit Fraud: Rental deposit fraud is very common nowadays where scammers request upfront payments or deposits without showing the property or providing proper documentation. To safeguard against this, remember that a good landlord will want you to see the property and like it so that you live there for a meaningful period of time. Any pressure tactics from landlords are concerning. It is essential to exercise caution when dealing with landlords who ask for immediate payments or ask for wire transfers or prepaid gift cards. Always conduct your due diligence first, ensure ownership of the property, sign a written lease agreement before any deposits, use secure payment methods such as bank transfers or certified cheques and request receipts for any financial transactions.

Ensure you have proper documentation: Request written agreements that outline all terms and conditions, including rent, utilities, and deposit requirements. Ontario has a standard lease that landlords can use. You can review it here to ensure that the lease you are signing has all the important information. It is important to note that no deposits are required prior to signing a lease. Review contracts carefully and seek legal advice if necessary to clarify any ambiguities or concerns.

Protect your identity: Although there is plenty of personal information required on applications, there is no need to put your identity at risk. It has been seen in many cases that scammers steal personal information and use it for various fraudulent activities. Landlords will want information that includes your name, address, employer, income, previous place of residence, contact information of your previuos landlord as well as personal references and credit history. There is absolutely no need and no requirement to provide more personal information like your SIN number, drivers license number or any credit card numbers. If they have an application requesting that information, you can leave it blank and outline that as a general practice you avoid sharing that information because of the inherent risks and you are happy to work with them to ensure they feel comfortable and have all the information they need to make a decision. Landlords do not need your SIN number for anything.

As prospective Landlords will want to understand your credit history, you can work on a safe way to provide this. Most banks will provide you with access to your credit score and report and if your bank does not provide this, you can use a service like creditkarma. You can print out your credit report, black out the personal information and share a copy with your application.

In conclusion, while the rental market offers numerous opportunities for individuals seeking housing, it is essential to feel comfortable taking the steps required to avoid rental scams. By following these proactive steps and exercising due diligence, tenants can protect themselves and make informed decisions when navigating the rental landscape.

As a woman I know all too well about the many financial penalties we face. The list is long ranging from the gender pay gap (we earn $0.87 for every dollar a man earns), and the extra responsibility for children and family care (we spend an average of 3.9 hours per day on unpaid work, 1.5 hours more than men) to the pink tax where women routinely pay more than men for a variety of items ranging from mortgages to car repairs.

What I had not done was put this information together. I had never really thought about the collective impact of all these disadvantages.

That is until, I had the privilege of talking to Kristine Beese, founder of Untangle Money.

Kristine told me about how women get paid less than men (female dominated industries that pay less than male dominated industries and within each, women get paid less). At the lower end of the financial spectrum, this has significant implications on the health and wellness of women. It threatens quality of life, limits investments in enablers of success like education, and significantly increases risks for dependency. I have seen this first hand – my mother worked as a seamstress in a factory and was financially dependent on my father who was abusive.

At the higher end of the financial spectrum, it has significant financial implications. After reading Robyn Doolittle’s Globe and Mail article on the wage gap between female equity partners at top law firms, Kristine did some math. The article found that men at the equity partner level made an average of $371,596 more each year than women at that tier (a 25% pay gap). If the gap exists for 10 years and the money is invested at 4.5%, then it is worth $4.7M dollars.

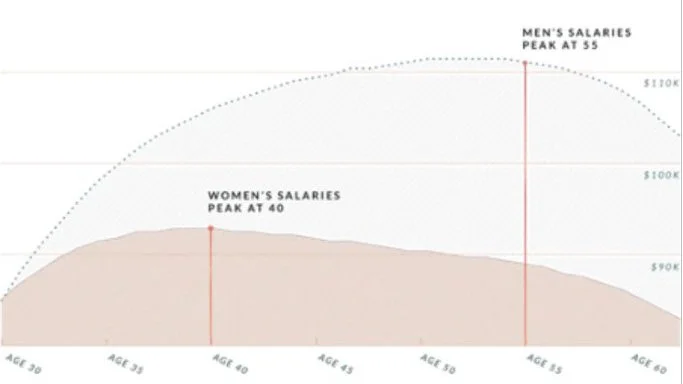

Kristine discussed how women’s salaries peak around 40 and men’s peak around 55 , creating many decades of higher salaries for men. She talked about how women hit middle management and struggle to get beyond, how women struggle with fitting in the networking and social activities that often lead to greater opportunities, how more wealth is passed down to men, how men make more financial decisions and how women spend less time in the workforce due to child and family care, receiving less in pensions and the list goes on….

Slide originally from Ellevest demonstrating salaries by age

When you put all of this together, women have a higher risk for financial struggles. The 2019 Canadian Financial Capability Survey revealed that women make up 60% of those Canadians who are struggling to manage their day-to-day finances.

So, the question becomes, how do we fix this.

From an individual perspective, we women need to step up and take ownership over our finances. We need to understand that this is happening to us. We have to take time to both figure out how and then push towards addressing it in our own lives. So that means everything from problem solving how to increase our incomes to actively managing our money and planning for retirement. Untangle Money can provide support on the latter and also shares great insights and perspective via social media and financial book clubs.

From a systemic perspective, we need to collectively address this. This is not an isolated issue and it is not the sole responsibility of under resourced women to build a fair and equal system for everyone. We need our political, public, private and not for profit sector leaders to recognize the financial resiliency of women as a key issue and dedicate meaningful resources to addressing it. Yes, that means budget increases to provide equal salaries and investments in pensions, collective investments in childcare, and financial capacity building. It also means a shift to intentionality. We can build a fair and equal society by deeming it important and intentionally prioritizing our resources to make it happen.

Sources:

1. Gender pay gap: https://canadianwomen.org/the-facts/womens-poverty/

2. Unpaid work: https://www.theglobeandmail.com/canada/article-power-gap-backstory/

https://www150.statcan.gc.ca/n1/pub/89-503-x/2015001/article/54931-eng.htm

3. Pinktax: https://www.chatelaine.com/living/10-things-canadian-women-pay-more-for/

4. Gender pay gap at legal firm: https://www.theglobeandmail.com/canada/article-wage-gap-between-male-female-equity-partners-at-top-law-firm-averages/

5. Women's higher risk for financial struggles: https://canadianwomen.org/the-facts/womens-poverty/

Financial resiliency is one of those things that requires focus on the day to day money challenges as well as the ability to step outside of the frame to see the whole picture. If we don’t do this, we get stuck with the day to day and struggle to figure out the best way forward.

I feel very grateful to have interviewed Kathryn Meisner. She is a career and salary negotiation coach. She has worked with 500+ people. This helps her constantly step out of the day-to-day and see the whole picture. It helps her see what employers are looking for, what language they are using, how they make hiring decisions, what they are paying for what level of work and how to best negotiate. It also helps her see what employees are struggling with, what works and what does not. I can instantly see the value of having Kathryn, her strategic approach and macro level insights in your corner.

I learned 3 foundational yet game changing insights from my discussion with Kathryn.

1. We can accelerate successes by creating momentum and we can accelerate momentum through focus: Although this seems intuitive, we often forget that we can harness and work with our momentum. Kathryn talked about how her process is designed to move people forward. One of her clients’ first action items - when commitment and momentum is highest - is to complete a detailed questionnaire. Participants then draw upon that content throughout the rest of their career exploration and job search journey. She also describes how a lot of her work is helping participants create momentum by establishing gates for decision making. Often times, the information gathering process can lead to analysis paralysis. Kathryn helps participants focus on what they need to make the decision and move forward. Some strategies that we can use to create momentum if we can’t work with Kathryn include:

Setting up deadlines & accountability. For example, let a friend know that you are working on a career pivot, you would value their feedback on your approach and would like to set up a coffee date to go over it. This forces you to be ready by the coffee date.

Bounding the amount of research before a decision. For example; I will look at the pay of 10 jobs in the field I am interested in and speak to 5 people about how they negotiated their salary. Once I do this, I will set my target salary.

2. We can accelerate our success by being clear on what we want. This means that getting to our goals, be it a new job, a higher salary, a role that uses specific skills or a family friendly culture requires clarity on the specifics. Kathryn compared this to apartment / house hunting. You need enough specifics to enable selection. So, in the case of an apartment, you may need a budget, desired location and amenities. In the case of a career change, you need to deeply understand what keeps you feeling engaged and fulfilled in addition to your salary needs. Everyone is different. Some people really want to use specific skills, others have a certain impact, others want to work with a certain group of people or earn a certain amount. Clarity on what you want helps you avoid spending a lot of time going in circles or even worse selecting something that doesn’t work, meaning you can avoid going through the process all over again.

3. We can accelerate success by re-thinking and re-framing our experience and approaches. Kathryn works with many clients who have non-linear career paths or struggle to demonstrate the value of their work. Employers often look to job titles, resumes and relationships for signs of value. This puts those with a certain level of privilege at an advantage. Kathryn strategically points out that by understanding the system, you can work it to your advantage. First, knowing the desired skills of a role enables you to think about how you have demonstrated these. You may not have been a Project Management Director, but you could have been project managing a household, volunteering, or working multiple jobs through school. Or you may not have had direct reports but you have been managing stakeholders to move projects forward from multiple departments and that may have included ensuring recognition and capacity building - skills associated with people management.

Overall, there is often an opportunity to step back and re-think our approaches. We frequently start things by doing what we know. So, when looking for a job, we may update our resume and look for postings. The truth is that we are seeing fast paced change and new approaches that can be much more effective. Kathryn’s approach is all about engagement, coffee chats, informational interviews. It is exploration and gathering information while building relationships and connections with those in a space you want to enter. It is in essence research in parallel with targeted marketing. Re-thinking our approach can lead to better and faster wins.

Overall, I want to thank Kathryn for her very helpful insights. She recognizes the privilege associated with career navigation and the emotional, human and financial resources required to transition. She openly shared her perspectives for those who cannot afford to have her directly in their corner. She has also created some great free resources including an email course to help you figure out your next step, a job search checklist and a salary negotiation guide for women. For those that can, I certainly see the value of her coaching work. She has set up a valuable ecosystem to support an accelerate success. And she deeply cares about the success of her clients.

he important question is what is our recipe for all Canadians to thrive? I believe Paul Taylor, Executive Director of FoodShare has insight into the right ingredients.

In his recent interview published in LiisBeth, he discusses his focus on implementing standard-of-living wages and a wage compression policy where FoodShare has tied compensation for the lowest wage worker to the highest. This means that the Executive Director can make no more than three times what the lowest paid worker makes.

These are critically important initiatives – they ensure that people are valued for their contribution and not their power to influence the allocation of resources or their ability to forego lower paid jobs and invest time and money in accessing higher paid employment.

Even more importantly, they demonstrate FoodShare’s commitment to a socially just future and enable the organization to drive change in a manner that is consistent with desired outcomes. I believe commitment and congruence between actions and outcomes are 2 core ingredients in the recipe for building a society that enables all Canadians to be financially resilient and thrive.

Sometimes I think of financial resiliency as a real-life Super Mario game. In the video game, you are trying to move forward and get bombarded with piranha plants, ice boulders, firebars. In real life, there is precarious employment, skyrocketing housing costs, post-secondary education, privilege, systemic racism, loaded dice, fixed fights.…. It often seems Leonard Cohen might be right in saying “everybody knows, the poor stay poor, the rich, get rich”.

Richard is a 25-year-old living with a roommate in Toronto. He previously worked in the restaurant industry earning enough to support himself and enjoy some travel. Like many Canadians he has lost his job and has been surviving on government supports. He decided to start taking some university courses this September given that he was home. He is increasingly getting concerned about his future and how to make ends meet once government supports end.

A recent analysis by the Canadian Centre for Policy Alternatives (CCPA) found that “while millions of Canadians lost their jobs because of the COVID-19 pandemic, “the country’s top 20 billionaires have amassed an average of nearly $2 billion each in wealth”[1]. It’s not only the ultra-rich that are doing well. Those of us with jobs are not spending our money on gas, 407, evenings out or holidays. In addition, if we have wealth generating assets - we have mostly seen an increase in their value. Average Canadian home prices were up 17% in December 2020 vs the same period in 2019[2] and although the S&P/TSX Composite Index dropped 37% during the year, it climbed back up to finish the year with at 2.17% gain[3] while the S&P 500 delivered a 16% return over the previous year[4]. This indicates that lower income Canadians without financial or real assets are bearing the brunt of the economic consequences associated with COVID-19.

Happy New Year! We have made it through and we seem to be climbing our way out of the ever spiraling hell in a hand basket disaster that was 2020.

As I think about the coming year, still full of health and financial challenges, I have been trying to hone in on what is needed to make it the best that it can be. Knowing that we will need to work our way out of this hole, how can we make the most of it. What are those ingredients that are most valuable to invest in?

Based on my research and Strive work, I believe there are the three core ingredients to setting a path towards success regardless of the unexpected landmines life may throw: Empathetic Understanding, Focus, and Practice.

Emphatic understanding opens the gate to constructive action, Focus enables us to direct our efforts towards specific goals and Practice provides the action and repetition required for impact. I believe that together these ingredients can help make 2021 the best possible year whether you are an individual struggling to figure out how to make ends meet, jump into a higher paying job, a new immigrant trying to develop a financial plan or a support provider helping clients deal with financial emergencies.

Let me explain each one.

Empathetic understanding

We are bombarded with a breadth of messages on how we can be better and do better with our money. Although articles like this recent Forbes one on How to Find Financial Stability in Uncertain Times provide good insights around having a plan, cutting costs, and building up cash savings, they fail to provide an understanding of the real context we are in.

The reality is that Canadians were struggling before the pandemic. We struggled with housing affordability, precarious work and increased debt. These struggles are the result of a macro level trends that are far beyond an individual’s ability to control their finances.

Covid19 has taken this reality and created a financial crisis for certain segments of our population. According to a recent Toronto Star article, 15% per cent of individuals earning less than $22 an hour are laid off or working fewer than half the hours they did in February, while the rest of the workforce has more or less fully recovered.

We need to truly understand context and that everyone’s context is different. We need an empathic understanding of our individual context and that of others. This is key to constructive action. It helps stop the shame of not being where one wants to be. It provides the space for problem solving, creativity and innovation. It is what helps us figure out seemingly intractable problems.

With empathetic understanding in place, we can move onto:

Focus

Here we can allow ourselves the space to think about what we truly want. We can dream and envision where we would like to be. We can focus and sit with our goals, truly understanding the time and financial investment required to achieve them. We can then problem solve and develop strategies that will effectively move us forward.

Practice

Once we have focus and clarity, we can invest in practice. Any journey towards a particular goal requires change - if our actions do not change, then our results will not change. And change is hard, it requires moving out of autopilot and investing in thinking, learning, building new processes, testing, and refining our approach. So, if you are a low income single parent, practice could involve carving out an hour each week to learn strategies others low wage earners have used to transition to higher income. If you are a stretched service provider with no resources, practice could involve carving out time to interview individuals from other organizations or departments to understand possibilities for moving forward.

With practice one can slowly but surely invest in new strategies, figure out what works and what does not, and take meaningful steps forward. It is these steps that will help us slowly build success despite the craziness that life throws at us.

I hope that 2021 brings us all a healthy dose of emphatic understanding, focus and practice.

Finishing up school can be both exciting and scary. It is a celebration of years of learning, studying and plain old hard work. It is also the entrance into the ever-changing world of work. With youth unemployment rate at 11%[1], this can be daunting. From side hustle to precariousness to endless job applications, figuring out the best way to build a career is like a challenging maze at best.

I spoke to Dianne about student success strategies, common pitfalls and the breadth of resources available to support students in career planning and am sharing her insights below.

The ongoing COVID-19 pandemic is shining a light on financial precarity among Canadians. Prior to this crisis, 44% of Canadians said it would be difficult to meet their financial obligations if their pay was late, and more than 1 in 10 families with debt skipped or delayed a non-mortgage payment. COVID-19 has had an enormous impact on our economy, with 5.5 million Canadian workers affected by the shutdown between February to April. The unemployment rate was at a “record high” of 13.7% in May.

On the individual front, peer-to-peer interventions may have potential. They can build individual capabilities, address issues of shame, and support individual action. They can help individuals manoeuvre complicated administrative systems and build self-advocacy skills. In time, taking part in such interventions could help support people to join movements that lead to system change.

In a span of weeks, the Covid19 crisis has wreaked havoc on our health systems, communities and economy. It has unmasked the pre-existing vulnerabilities and inequalities in our system.

The risks of contracting the coronavirus and the individual impacts of the collective crisis vary greatly. At one extreme, you have individuals and families whose net worth has been pummeled by a drop in the stock market, yet still have the financial means and or secure employment to isolate themselves comfortably, order food, and wait out the crisis. At the other end of the continuum, you have 53% of Canadians who live paycheque to paycheque. This group is over half of our population and is made up of a wide variety of individuals and families.

The rent vs buy debate has been a long-standing debate with lots of calculations and heavy opinions. I have had my own personal thoughts but have never really weighed into the debate. In spirit of full transparency, I have a personal affinity towards the buy side. I bought early in my life and have benefited from that investment by being able to build equity and then leverage that equity for further investments. In all truth I had never really done the full math comparison before this but recently my husband sent me a Globe & Mail article; How the 5% rule changes the rent vs buy debate and I was curious so dug in…

The premise of the article, and focus area in most other articles I have subsequently read is that we should calculate the unrecoverable costs of each option in order to assess which is better. I find this approach to be simplistic and somewhat misleading for such a critically important question.

Yes the costs you can’t get back (fuller explanation at the end of this post) are important but so are these considerations that are missing from all discussions I have seen;

1) Your return on real estate is on the full value of the property not just the down payment that is your money;

2) Real estate can help you build capital in a way that no other investment can; and

3) Buying a home can help build resiliency

Let me dig in a bit more…

1. Your return on real estate is on the full value of the property not just the down payment that is your money. When you buy a house you save up a sum of money and use that for a down payment on the house. The bank lends you the rest of the money and you pay the bank back with interest. For example, let’s say the house is $500,000 and you put in $50,000 or 10%. Over a period of years, let’s say 25, you pay back what you borrowed from the bank via your mortgage. During this period your house appreciates in value, the article had a figure of 3% annually based on historical performance of real estate. So after 25 years you have a property worth $1,046,888.96 (calculator link included). What is important to note is that you only put in $50,000 so you are gaining a return on your money as well as the money the bank lent you. The 3% compounded annual growth on real estate of $500,000 is actually $12.94% (calculator link included) compounded annual growth on your $50,000 down payment.

Had you taken your $50,000 and earned 3% only on that, you would have had $104,688.90. Had you taken that $50,000 and put it in stocks, using the 6% annual return figure used in the article, you would have $214,593.54. Yes that is significantly more than if you put your $50,000 in savings, but in real estate, you earn money on the entire house so that makes your return significantly higher. You do have to take into consideration the money you pay to the bank for your mortgage - let’s say 5%. That still leaves you at a rate that is pretty competitive with stocks.

Now it is important to note that if your down payment is higher, your return drops – at $100,000, a 20% down payment, your return becomes 9.85% instead of the 12.94% above. So unless you are buying a house for cash, the actual rate of return will be higher than the real estate average rate because you can earn it on the full value of the property and not solely your down payment.

2. Real estate can help you build capital in a way that no other investment can. This consideration is particularly important if you do not have a meaningful amount of equity.

Financial insecurity in Canada is high with 44% of Canadians living paycheque to paycheque. Unfortunately I see this continuing because of a number of macro trends including:

The decline in secure well paid employment and an increase in precarious work – the average wage Canadians are paid per hour has hardly changed since the 1970’s

The growth in the amount of debt Canadians are carrying – Canadians now have the highest debt to income ratio in the G-7 at over 163%,

The levels of retirement savings - 32% of Canadians are nearing retirement without any savings

The shift to wealth being generated by capital instead of labour - according to Statistics Canada, net worth increased faster among families at the top of the income distribution, largely because of asset gains

Given these trends, being able to build capital is critically important for everyday Canadians. Realistically, individuals are no longer just going to save their way towards financial security. Outside of real estate, I cannot think of any other investment where an individual can leverage their existing assets at such a high rate for an extremely low cost.

From our example before, let’s say an individual invested $50,000 in the stock market and wanted to borrow against it to increase their investment pool with a goal of earning more money in the stock market. I bet it would be impossible to get a loan at mortgage equivalent rates, to invest in stocks. I can only see a bank providing $450,000 to someone with $50,000, so they can invest it in the stock market on a summer hot February 30th.

Figuring out how to get into the market via real estate can help you build the capital you need to fully participate in the wealth generating mechanisms of our economy. It can help build your ability to generate wealth outside of income. I cannot think of any alternative investment that can do that at that scale.

3. Buying a home can help build resiliency. Over the years, I have found that buying vs renting can help build resiliency in the long run. Want to accelerate your savings to travel, support your kids education or build up your retirement fund? Well there may be many more options with a home. You can rent out your basement or rooms in your home. I know individuals who have lived in the basement and rented the upper part of their house to pay down your mortgage faster. Want to spend a year traveling and not have to come back and be faced by exorbitant rental rates because you are no longer covered by rent control? You can rent out your home and build equity while you travel. If you can afford to buy and make your mortgage payments, there is a value in helping you be more resilient.

Rent vs Buy

So where do we net out?? It is a personal decision that each individual is best positioned to make when they have perspective of the full implications of each option. If you are interested in or see yourself relocating, the transaction and other costs associated with selling and moving may significantly erode the financial value of buying. If you have a strong dislike for DIY, multiple projects and having to maintain a property, then renting is for you. Alternatively, if you have a goal of increasing your financial independence, and security then buying can help you build that initial equity and wealth very well.

That is all well and good but how do you afford to buy???

No doubt that the prices have increased making the initial home purchase harder than ever. Given the above considerations, and current trends which are signalling continuation in affordability challenges, I think there is value in investing time in thinking of your personal goals and possible creative solutions ranging from co-ownership to purchasing of a rental property in order to get into the market before giving into the rent side.

What is important is that everyone consider all the implications of their decision and work to mitigate the risks associated with each option. Take the time to understand and think about what is best for you. Then you are free to build a plan to move forward and mitigate any risks.

Unrecoverable costs

All the costs you pay that you won’t get back, so rent on the rent side and property tax, maintenance costs and the cost of capital (mortgage interest) on the buy side. Basically the 5% rule is that if you can rent for 5% less than mortgage payments then doing so would be a sound financial decision. The 5% is a rough estimate calculated using estimates for unrecoverable costs (1% for property taxes on a house you buy, 1% for maintenance costs, and 3% for capital costs and the opportunity costs of not having your money in stocks – historically stocks have grown at a higher % than real estate).

If we think about this in terms of personal finance, being able to achieve one’s goals is dependent on skillfully managing a significant number of areas. These range from having a plan that advances towards our goals, creating a budget for those goals and ensuring we stick to that budget, to honing in on careers and jobs that are fairly well remunerated, negotiating our salaries, using debt to help us not hold us back and making wise investments with the money we do have.

Each of these areas is unique and requires a breadth of different skills and activities. So developing a plan that gets me to my goals requires me to spend time thinking about the life I would like to lead, researching and understanding the costs associated with that life, having clarity on my passions, skills and resources so I can figure out how I can pay for it, and learning about how others have gotten there. Some of the key skills here are self-awareness, critical thinking, planning and problem solving.

We know the struggles students face with tuition fees increasing 40%[1] in the last decade, increase in precarious work and frozen minimum wages that are far from living wages.

In trying to help students succeed within this challenging environment, Strive has been identifying and sharing strategies students are using to manage their money and achieve their goals. We hosted Finesse Your Finances at York University and gathered great insights into what students are doing today to set themselves up for success.

In interviewing Alyssa, she discusses the importance of self-advocacy in success. She says, “In some of our greatest struggles, we find our greatest strengths”. Advocating for ourselves can help us find those greatest strengths.

Here are 5 easy steps that can help you flex your self-advocacy muscles and make progress towards your goals.

The World Economic Forum predicts that it will take 170 years for economic parity to be achieved[2]. What are our plans to close the gender wage gap in under 170 years?? In the spirit of meaningful progress, I have highlighted three meaningful actions most individuals within an organization we can take to advance the issue.

We’ve all seen the numbers - the housing market is racing forward as incomes are left in the dust with little to no growth and an increase in precarious work. A member of my Strive group recently asked for some insights on how to get into the housing market. I thought back to the many Strive interviews I have conducted as well as my experiences and pulled together a top 6 list that may be helpful if you are in the process of trying to make that leap.